Full Sail Partners Blog

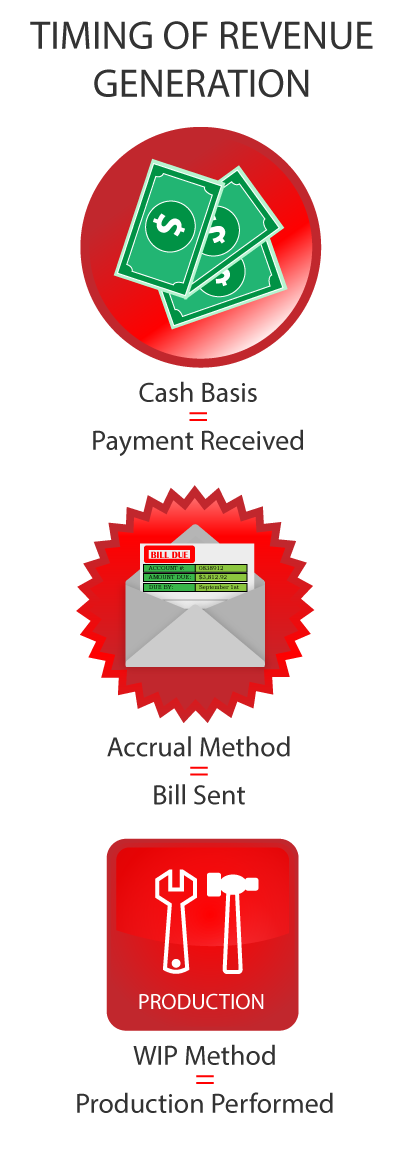

The timing of when you recognize revenue for your business can be influenced by a number of factors. In normal day-to-day business, most firms use a revenue generation model that recognizes revenue on an accrual basis – revenue hits the books and project reporting when clients are billed for services rendered. For tax purposes, revenue is not generally recognized until the client pays for the services rendered (cash-basis accounting).

The timing of when you recognize revenue for your business can be influenced by a number of factors. In normal day-to-day business, most firms use a revenue generation model that recognizes revenue on an accrual basis – revenue hits the books and project reporting when clients are billed for services rendered. For tax purposes, revenue is not generally recognized until the client pays for the services rendered (cash-basis accounting).

In addition to standard accrual and cash basis recognition of revenue, many firms are interested in recognizing revenue at the time services are performed. That revenue is then tracked on the project and financial statement as either unbilled or billed revenue. This article will focus on those revenue methods that recognize the value of your qualified Work In Progress (WIP), as unbilled revenue. Additionally, the methods described, will allow unbilled revenue to be reported on project reports and on your financial statements.

A word of caution! Before changing your method of revenue recognition, you should meet with your tax professional to discuss the requirements for your firm and discuss industry standard revenue recognition methods to determine right method for your firm. Also, you will want to meet with the owners of the firm, as well as, the project and divisional managers to discuss their requirements for financial and project reporting in regards to recognizing unbilled revenue.

Enabling Revenue Generation

As revenue generation posts revenue to your financial statements, you will need to create at least two general ledger accounts:

-

Unbilled Services (asset – balance sheet)

-

Unbilled Revenue (revenue – income statement)

The unbilled services account will carry the job-to-date unbilled revenue amount for your projects. The balance in this account will be carried over from one fiscal year to the next. The unbilled revenue account will carry the year-to-date unbilled revenue amount for your projects and the balance will be cleared to retained earnings at the end of each fiscal year. At all times you should be able to balance the detail on your projects to the balances in your GL accounts. This is called file reconciliation and it is very important that you reconcile these balances on an on-going basis. When performed properly, revenue generation will never cause a file reconciliation issue.

In addition to the general ledger accounts, you will need to establish and setup revenue methods to be used in the revenue generation process. These revenue methods will be specified at the lowest level of your project setup so that the work performed on those project levels can be recognized as revenue. We will be using two revenue methods in this discussion:

-

Method “W”, which calculates Total Revenue as Job-to-Date (JTD) Billed plus WIP at billing rates

-

Method “B”, which calculates total revenue as JTD Billed

Note: the Revenue Generation Method is used to calculate Total Revenue. Billed Revenue is then subtracted from Total Revenue to calculate Unbilled Revenue.

To determine which revenue method to use, this decision should be made on a project by project and phase by phase basis. You will only want to recognize revenue on those projects and phases where you expect to be able to bill and collect on your work effort. Also, you may need to set limits on your revenue generation methods so that revenue is not calculated above and beyond your contractual limits with the client. In some cases, Method W might be used on one or more phases in a project and Method B is used on other phases within the same project. Additionally, the method used may need to be changed as a project reaches a fully billed status.

Running Revenue Generation

The following should be completed, before running and managing revenue generation:

-

Determine your revenue methods

-

Create your GL accounts

-

Create your revenue methods

-

Setup these revenue methods in your projects

We recommend starting with a small sample of projects, testing your revenue generation methods, and procedures on these projects before expanding to all billable projects. Keep in mind that you can use Method “B” on some projects, which will keep them on an “Accrual” basis where revenue = billed.

Part of the management of Revenue Generation is the creation of good reports to check your “baseline” prior to generating revenue. Then check the reports again after generation of revenue and after billing. A report should be created showing the Contract Amount, Billed Revenue, Unbilled Revenue and Total Revenue at a minimum. This report can be run at the project level to verify overall amounts and/or at the phase level to verify individual phase level amounts.

Revenue Generation should be run at the following times and for the following reasons:

-

Each week after posting time and expense | Ensures revenue is generated and can be viewed on reports

-

Month end, prior to billing | Verifies the total of unbilled revenue for the month can be viewed

-

Immediately after billing | Confirm billed and written-off amounts are properly recorded and unbilled revenue is verified as total revenue less billed revenue

Verifying and Managing Revenue Generation

As mentioned above, Revenue Generation should be run following billing and the unbilled revenue. The remaining unbilled on reports should be compared to the general ledger balance (in the Unbilled Services asset account) and to unbilled detail and summary reports. If there are any projects where the unbilled amount does not seem right, run a project detail report to see all individual transactions and billing statuses to determine where the discrepancy might be.

One action that might cause unbilled to be different than expected would be where you process a fee based invoice for less than the unbilled amount of labor and do not put any of the labor on hold prior to billing. In this type of situation, you might bill $5,000 on $6,000 worth of labor and expect there to be $1,000 of WIP remaining. However, if you processed the invoice without putting any of the labor on hold first, then all $6,000 of labor would be cleared as having been billed against the $5,000 fee and you would not have any WIP remaining.

Another item to keep in mind is that the billing process does not have any effect on total revenue. The process of billing simply moves revenue from Unbilled to Billed. When using Revenue Generation, revenue is only generated when Revenue Generation is run, not at time of billing.

General Ledger effect when generating revenue:

-

Debit to Unbilled Services

-

Credit to Unbilled Revenue

General Ledger effect when running billing:

-

Debit to Accounts Receivable

-

Credit to Unbilled Services

-

Credit to Billed Revenue

-

Debit to Unbilled Revenue

To learn more about revenue recognition, join our webinar as we discuss the 9 key points to keep in mind regarding Revenue Generation.