KPI - the New Industry “Buzz” Word

A KPI, or Key Performance Indicator, is a measurable value that demonstrates how effectively a company is achieving crucial business objectives. Organizations should use KPIs to evaluate their success at reaching targeted goals. Simply stated, KPIs provide your firm with metrics that compare budgeted amounts to the actual values. KPIs are no longer just for accounting and finance as they now reach deeper into a firm’s operational side examining marketing, business development and project management.

A KPI, or Key Performance Indicator, is a measurable value that demonstrates how effectively a company is achieving crucial business objectives. Organizations should use KPIs to evaluate their success at reaching targeted goals. Simply stated, KPIs provide your firm with metrics that compare budgeted amounts to the actual values. KPIs are no longer just for accounting and finance as they now reach deeper into a firm’s operational side examining marketing, business development and project management.

KPIs vs Traditional Reporting Methods

Let’s take a look at how firms benefit from KPIs and how KPIs differ from standard reporting. A common reporting technique is to compare current profit & loss results to the same period the previous year, or to compare year to date then versus year to date for the current year. Budget data for one or both comparisons can be incorporated. Now, what if we graphed this information and included a desired growth line? We will then have a visual of actual performance in relation to a chosen measurement. This measurement will inherently become an indication of whether we are achieving our goals, and would allow us to be proactive in correcting potential challenges.

Using KPIs to Measure Success

As mentioned earlier, KPIs are not just a tool for the finance team. For example, a chief operating officer may not relate well to traditional financial statements and focusing on project related metrics would be more to his liking. These indicators can be project specific, relate to a grouping of projects, or be sliced and diced based on the organizational breakdown structure (OBS) or work breakdown structure (WBS). Click here to learn more about OBS and WBS.

In another scenario, a chief strategy officer believes there is a benefit from evaluating trending data regarding hit rates filtered by a predetermined criterion. However, we must keep in mind that unless a benchmark or some other distinguished metric is established, this may not result in a clear and meaningful measurement.

Here are two examples of KPIs that have proven to be successful:

- Cost and Schedule Variance – Using Deltek Vision reporting, actual project cost performance index (CPI) and schedule performance index (SPI) is calculated and compared to an acceptable mean-variance.

- Estimate at Completion (EAC) Analysis – This can be as simple as a two-column report showing EAC in comparison to the contract value. The criteria can also be set by contract type to “flag” anomalies that need to be further investigated.

The Bottom-line on KPIs

KPIs can be used company wide. C-level executives can look across client and project types and evaluate revenue multipliers or collections success. These same evaluations can be done at all levels across your enterprise from managers that are accountable for sections of your organization down to individual project managers driving the lowest levels of WBS. What is required is a benchmark, a budget or a goal. Whether top down or bottom up, the view into why businesses perform the way they do will kept top of mind.

So, how does your firm measure success across the enterprise? Is it profit centers, projects, employees or pursuits? Every firm is unique and can’t just use “off the shelf” KPIs. It all begins with a discussion of what you need to drive your firm to the finish line. Once decided, designing the reports and data is easy.

Spend Management is a popular term, but what is it really? Spend Management can encompass anything from procurement, supply chain management, expense control, outsourcing and more. For most businesses, managing spending may not seem to provide a competitive advantage nor differentiate them from the competition. While this task doesn’t directly drive revenue, figuring out how to better manage and control your travel costs, expenses and invoicing does provide significant business value.

Spend Management is a popular term, but what is it really? Spend Management can encompass anything from procurement, supply chain management, expense control, outsourcing and more. For most businesses, managing spending may not seem to provide a competitive advantage nor differentiate them from the competition. While this task doesn’t directly drive revenue, figuring out how to better manage and control your travel costs, expenses and invoicing does provide significant business value.

Within Deltek Vision lies a very handy tool, which enables a firm to have multi-company functionality. However, the benefits of this multi-company functionality feature seem to elude many firms that would greatly appreciate its capabilities. So let’s talk in detail about multi-company functionality and the why, when and how firms should use this fantastic feature.

Within Deltek Vision lies a very handy tool, which enables a firm to have multi-company functionality. However, the benefits of this multi-company functionality feature seem to elude many firms that would greatly appreciate its capabilities. So let’s talk in detail about multi-company functionality and the why, when and how firms should use this fantastic feature.

Don’t be a headless chicken running around trying to get through the year-end process. Let’s review some considerations and tips to make your year-end close just a little easier.

Don’t be a headless chicken running around trying to get through the year-end process. Let’s review some considerations and tips to make your year-end close just a little easier.

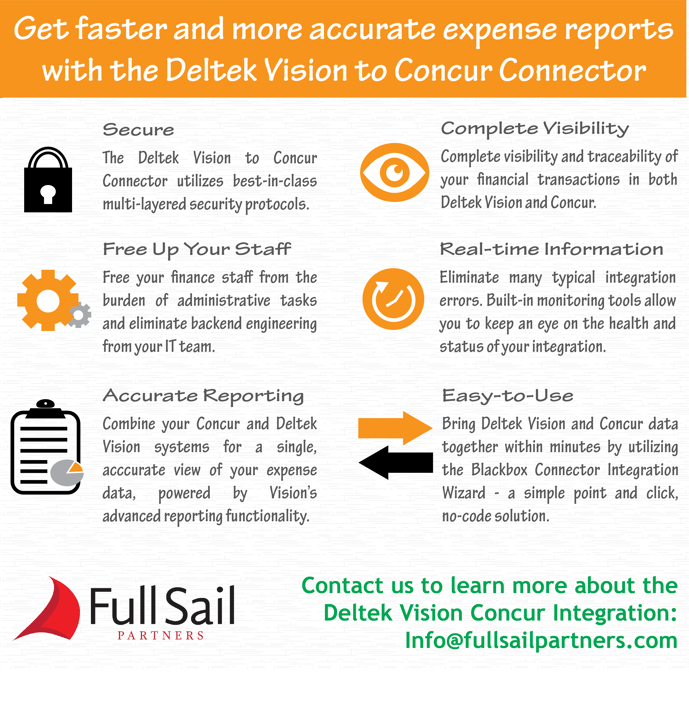

The Deltek Vision to Concur Connector allows both systems to work together seamlessly, automatically synchronizing finance data throughout the entire spending process, from pre-spend approval to reconciliation. Manage every expense and invoice transaction accurately and with ease, and get a complete view of your finances in one place.

The Deltek Vision to Concur Connector allows both systems to work together seamlessly, automatically synchronizing finance data throughout the entire spending process, from pre-spend approval to reconciliation. Manage every expense and invoice transaction accurately and with ease, and get a complete view of your finances in one place.

For project-based firms, measuring current firm performance is the most significant indicator of future firm performance. Furthermore, by using trend data, firms can forecast cost and schedule variances in the early stage of a project. A preferred method by project managers to factor this trend data is the earned value management technique.

For project-based firms, measuring current firm performance is the most significant indicator of future firm performance. Furthermore, by using trend data, firms can forecast cost and schedule variances in the early stage of a project. A preferred method by project managers to factor this trend data is the earned value management technique.

Deltek is at it again! With the introduction of Deltek Vision version 7.6, professional services firms are now able to streamline their credit card processes thanks to several new key enhancements. Providing some background, the introduction of credit cards was one of the many improvements to Vision in version 7.3. When 7.3 was released, firms gained efficiency with employee expense reporting as employees could import charges from the credit card company. This feature allowed employees to associate those charges within their expense reports. Now, based on user feedback, credit card functionality has been expanded.

Deltek is at it again! With the introduction of Deltek Vision version 7.6, professional services firms are now able to streamline their credit card processes thanks to several new key enhancements. Providing some background, the introduction of credit cards was one of the many improvements to Vision in version 7.3. When 7.3 was released, firms gained efficiency with employee expense reporting as employees could import charges from the credit card company. This feature allowed employees to associate those charges within their expense reports. Now, based on user feedback, credit card functionality has been expanded.

I don’t know anyone that actually enjoys completing their expense report. The process is arduous, and steals valuable time from your already hectic day. The fact is, if you want to get reimbursed for a company expenditure, you have to take the time to complete your expense report. No ifs ands or buts about it. Luckily, Blackbox’s Deltek Vision and Concur Integration eliminates this pain staking process for your employees and frees them up to concentrate on client-focused, billable work.

I don’t know anyone that actually enjoys completing their expense report. The process is arduous, and steals valuable time from your already hectic day. The fact is, if you want to get reimbursed for a company expenditure, you have to take the time to complete your expense report. No ifs ands or buts about it. Luckily, Blackbox’s Deltek Vision and Concur Integration eliminates this pain staking process for your employees and frees them up to concentrate on client-focused, billable work.

Our first inclination when the new FASB 606 was announced was this wouldn’t impact many of our Deltek Vision clients. But after more insight, we recognize this has a tremendous impact on our clients. The rule states applicability to ALL entities that deliver goods or services. Though many believe that GAAP, FASB, SOX and other guidelines are good rules to follow regardless of any statutory relevance, the reality is if we are not being overseen we tend to be somewhat lax in compliance.

Our first inclination when the new FASB 606 was announced was this wouldn’t impact many of our Deltek Vision clients. But after more insight, we recognize this has a tremendous impact on our clients. The rule states applicability to ALL entities that deliver goods or services. Though many believe that GAAP, FASB, SOX and other guidelines are good rules to follow regardless of any statutory relevance, the reality is if we are not being overseen we tend to be somewhat lax in compliance.